Further to Customs Notice CN19-24 pertaining to Cannabis - Edibles, Extracts and Topicals Customs Excise Duty Procedures https://www.cbsa-asfc.gc.ca/publications/cn-ad/cn19-24-eng.html please note the following for completion of the CADEX formatted records:

- The table below is a list of the province/territory HS Administrative Codes to be entered in Field 27 on Form B3-3, Canada Customs Coding Form.

|

Province / Territory |

HS Administrative Code |

|

Alberta |

0000.99.99.70 |

|

British Columbia |

0000.99.99.71 |

|

Manitoba |

0000.99.99.72 |

|

New Brunswick |

0000.99.99.73 |

|

Newfoundland & Labrador |

0000.99.99.74 |

|

Northwest Territories |

0000.99.99.75 |

|

Nova Scotia |

0000.99.99.76 |

|

Nunavut |

0000.99.99.77 |

|

Ontario |

0000.99.99.78 |

|

Prince Edward Island |

0000.99.99.79 |

|

Québec |

0000.99.99.80 |

|

Saskatchewan |

0000.99.99.81 |

|

Yukon |

0000.99.99.82 |

- The table below is a list of the Proposed Excise Duty Rates for Cannabis Edibles, Cannabis Extracts (including Oil) and Cannabis Topicals

|

Province/Territory |

Federal Rate |

Additional Rate in Respect of |

Current Ad Valorem Sales Tax |

|

($/mg of total THC) |

Province/Territory |

Adjustment |

|

|

($/mg of total THC) |

(%) |

||

|

Alberta |

0.0025 |

0.0075 |

16.8 |

|

British Columbia |

0.0025 |

0.0075 |

- |

|

Manitoba |

0.0025 |

N/A |

- |

|

New Brunswick |

0.0025 |

0.0075 |

- |

|

Newfoundland and Labrador |

0.0025 |

0.0075 |

- |

|

Northwest Territories |

0.0025 |

0.0075 |

- |

|

Nova Scotia |

0.0025 |

0.0075 |

- |

|

Nunavut |

0.0025 |

0.0075 |

19.3 |

|

Ontario |

0.0025 |

0.0075 |

3.9 |

|

Prince Edward Island |

0.0025 |

0.0075 |

- |

|

Quebec |

0.0025 |

0.0075 |

- |

|

Saskatchewan |

0.0025 |

0.0075 |

6.45 |

|

Yukon |

0.0025 |

0.0075 |

- |

- The following example illustrates how the customs duty, federal excise duty and provincial excise duty is to be calculated on Form B3-3, Canada Customs Coding Form.

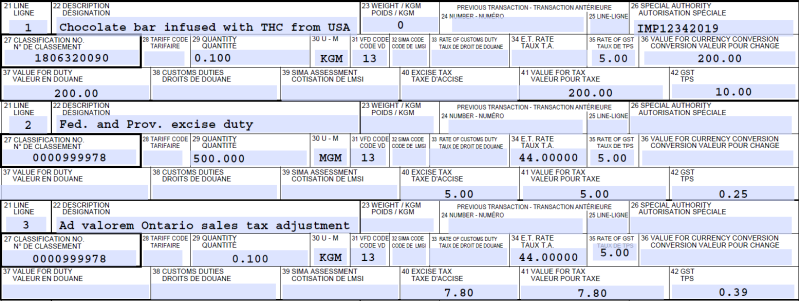

Example:

Calculation of cannabis duty and additional cannabis duty on a chocolate bar (U.S. origin), 100 grams, infused with 500 milligrams of THC imported in Ontario. The value of the importation is $200.00 (CAD).

Classification - Line 1

Shows the actual classification line; the Health Canada Import permit number must be entered in Special Authority field (26). The GST (5%) is calculated on the value for duty and entered in Field 42.

Calculation of Combined Federal and Provincial Excise Duty - Line 2

Shows the amount of the combined federal and provincial excise duty; this amount is calculated at $0.01 per milligram of THC of the quantity imported (which includes the flat-rate federal cannabis duty of $0.0025 per milligram of the total THC of the cannabis product plus the flat-rate provincial additional cannabis duty of $0.0075). See Table - Proposed Excise Duty Rates for Cannabis Edibles, Cannabis Extracts (including Oil) and Cannabis Topicals

- The importer is required to add the province/territory HS Administrative Code, for the province/territory of import in Field 27. See Table - List of the province/territory HS Administrative Codes

- The importer is required to enter 44 on field 34 – Excise Tax Rate to allow a manual calculation of Federal and Provincial excise duty to be entered in field 40 and THC quantity must be entered in field 29 of this line.

- The amount of the excise duty payable to be entered in field 40 is $5.00, this is calculated by multiplying 500 milligrams of THC by $0.01.

- This amount of $5.00 is also to be entered in field 41, value for tax.

Provincial Sales Tax Adjustment - Line 3

Shows the amount of sales tax adjustment for Ontario, calculated by multiplying the base amount by 3.9%. See Table - Proposed Excise Duty Rates for Cannabis Edibles, Cannabis Extracts (including Oil) and Cannabis Topicals

- The importer is required to add the province/territory HS Administrative Code, for the province/territory of import in Field 27. See Table - List of the province/territory HS Administrative Codes

- The importer is required to enter 44 on field 34 – Excise Tax Rate and manually calculate the sales tax adjustment amount to be entered on field 40.

- The sales tax adjustment amount to be entered in on field 40 is $7.80. This amount is calculated by multiplying the value for duty from field 37 of Line 1 ($200.00) by the provincial sales tax adjustment rate for the province of Ontario, which is 3.9%

- This amount of $7.80 is also to be entered in field 41, value for tax.

CADEX FORMAT

Line 1

- Prepare the first B3 line as you normally would to account for the goods

- The KI30 record would contain the Health Canada Import permit number in the Special Authority field

- The KI50 record would contain 00000001000 in the GST Amount field

Line 2

- The KI30 record would contain 0000999978 in the Classification Number field

- The KI40 record would contain 0000000500000 in the Classification Line Quantity field

- The KI50 record would contain 44.0 in the Excise Tax Rate field

- The KI50 record would contain 0000000500 in the Excise Tax Amount field

- The KI50 record would contain 000000000500 in the Value for Tax field

Line 3

- The KI30 record would contain 0000999978 in the Classification Number field

- The KI50 record would contain 44.0 in the Excise Tax Rate field

- The KI50 record would contain 0000000780 in the Excise Tax Amount field

- The KI50 record would contain 000000000780 in the Value for Tax field

- The KI90 record would contain 00000001280 in the Total Excise Tax field

- The KI90 record would contain 000000001064 in the Total GST field

- The KI90 record would contain 000000002344 in the Total Duty & Tax field