https://www.cbsa-asfc.gc.ca/publications/dm-md/d4/d4-1-5-eng.html

Ottawa, May 21, 2026

This document is also available in PDF (323 KB)

Plain language summary

Target audience: Importers of commercial goods, warehouse operators

Key content: The procedures to be followed by the Canada Border Services Agency (CBSA) in storing goods pending clearance or disposal

Keywords: accounting, commercial goods, importer, payment, storage of goods, warehouse, place of safe-keeping

On this page

- Updates made to this D-memo

- Definitions

- Guidelines

- Appendix A: Form E44, Notice – Unclaimed Goods

- Appendix B: Form E45, Inventory Control Log for Seized, Forfeited, Detained, Abandoned, and Unclaimed Goods

- References

- Contact us

Updates made to this D-memo

This memorandum has been updated to meet the Government of Canada’s accessibility standards, and to provide clarity regarding the annual adjustment of storage charges in accordance with the Service Fees Act and where to find current rates.

Definitions

"Act" means the Customs Act.

"Business day" means any day on which the customs office is open and accepts delivery or removal of commercial goods.

“CBSA Assessment and Revenue Management (CARM)” is a duty and tax collection system developed to modernize and simplify the process of importing goods into Canada.

"Commercial goods" means goods for sale for any commercial, industrial, occupational, institutional or other similar use that are imported into Canada or exported from Canada.

"Firearm" has the same meaning as in section 2 of the Criminal Code;

"Place of safe-keeping" means a place designated by the Minister pursuant to section 37 of the Customs Act for the safe-keeping of goods.

"Prohibited ammunition" has the same meaning as in subsection 84(1) of the Criminal Code.

"Prohibited device" has the same meaning as in subsection 84(1) of the Criminal Code.

"Prohibited weapon" has the same meaning as in subsection 84(1) of the Criminal Code.

"Restricted weapon" has the same meaning as in subsection 84(1) of the Criminal Code.

Guidelines

1. The Storage of Goods Regulations outlines how long goods may be stored in a customs office after they have been reported but before they are deposited in a place of safe-keeping:

- Standard time limit – 40 calendar days;

- Perishable goods – 4 calendar days;

- Prescribed substances under the Nuclear Safety and Control Act or General Nuclear Safety and Control Regulations – 14 calendar days;

- Firearms, prohibited ammunition, prohibited devices, prohibited or restricted weapons and tobacco – 14 calendar days; and

- Spirits – 21 calendar days.

2. The time limits for goods left in a place of safe-keeping, before they are forfeit are:

- Standard time limit – 30 calendar days;

- Perishable goods – 24 hours; and

- Prescribed substances under the Nuclear Safety and Control Act or General Nuclear Safety and Control Regulations – 24 hours.

3. The following locations are designated as CBSA offices in section 5 of the Customs Act:

- any location where CBSA maintains a business office;

- a CBSA detention yard; and

- a highway frontier examining warehouse.

Place of safe-keeping

4. The following locations may be designated as a place of safe-keeping:

- CBSA offices, highway frontier examining warehouses, King's warehouses;

- a portion of a sufferance or bonded warehouse; and

- any other place designated by a delegated CBSA official on behalf of the Minister of Public Safety.

Types of warehouses

Highway frontier examining warehouse

5. A highway frontier examining warehouse is one where goods, which are not moving inland by a bonded carrier to a sufferance warehouse, are held before they are released by the CBSA. These warehouses have been established at most points of importation adjacent to the Canada-United States international boundary and are operated by the CBSA. Goods which have been placed in a highway frontier examining warehouse must not be removed by the carrier or the importer until authorized to do so by CBSA.

6. Truck drivers may park vehicles overnight in CBSA detention yards if space permits.

King's warehouse

7. A King's warehouse is used to store seized, forfeited, detained, abandoned, and unclaimed goods before they are released or disposed of by the CBSA in accordance with the act. These warehouses are operated by the CBSA.

Sufferance warehouse

8. Sufferance warehouses are privately owned and operated facilities licensed by the CBSA for the control, short-term storage, and examination of in-bond goods until they are released by the CBSA or exported from Canada. More information concerning sufferance warehouses can be found in Memorandum D4-1-4: Customs Sufferance Warehouses.

Bonded warehouse

9. Customs bonded warehouses are used for the long-term storage of imported goods and are part of the Duty Deferral Program. Duties and taxes only become payable when the goods from a customs bonded warehouse are entered into the domestic market. Specific time limits can be found in Memorandum D7-4-4: Customs Bonded Warehouses.

10. There are two types of customs bonded warehouses:

- private warehouses, which are operated by individuals or companies to store their own imported goods; and

- public warehouses, which are operated by entrepreneurs to store goods from various importers.

11. More information can be found in Memorandum D7-4-4 and the Customs Bonded Warehouses Regulations.

Security of held goods

12. A delegated CBSA officer is responsible for ensuring the appropriate measures are taken in handling and safeguarding goods and vehicles stored in CBSA offices, highway frontier examining warehouses, King’s warehouses and CBSA detention yards.

13. Goods seized, forfeited, detained, abandoned or unclaimed under the act will be stored in a secure and controlled area, separate from other goods.

14. Unless moved to a King’s warehouse, the goods will be checked regularly and disposed of as soon as possible after the applicable retention period.

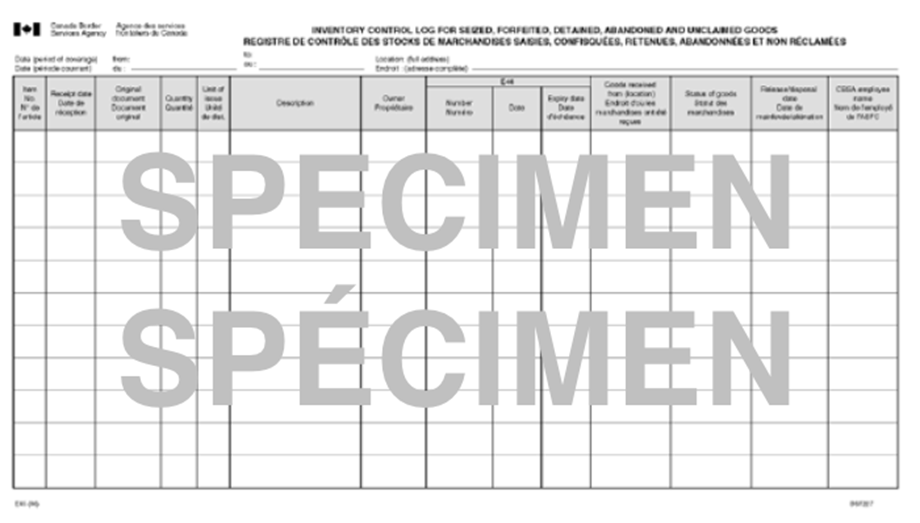

15. The CBSA will use E45: Inventory Control Log for Seized, Forfeited, Detained, Abandoned, and Unclaimed Goods (see Appendix B) to maintain an accurate record of held goods.

16. The Crown Liability and Proceedings Act includes information about damage claims and payment from negligence, a wrongful act, or a breach of duty on the part of an employee of the Crown. For damage or loss claims, contact the CBSA office concerned. The local CBSA office may contact their regional finance group for further information.

Storage of firearms and other weapons

17. Firearms must be stored in a container, receptacle, vault, safe or room that is securely locked and cannot be readily broken open or into, according to section 4(2) of the Public Agents Firearms Regulations.

18. Information about firearms and other weapons can be found in Memorandum D19-13-2: Importing and exporting firearms, weapons and devices, Customs Tariff, Criminal Code, Firearms Act, and Export and Import Permits Act.

Storage charges

19. Except under specific circumstances, storage charges apply to goods held in a place of safe-keeping, at a CBSA office, at a highway frontier examining warehouse, or at a King’s warehouse. For storage rates, refer to the “Schedule” in the Storage of Goods Regulations.

20. Please note that the text of acts and regulations on the Justice Laws website, including the Storage of Goods Regulations, does not reflect updated fee amounts resulting from automatic adjustments pursuant to certain acts or regulations, such as the Service Fees Act. For updated fee amounts, please refer to the most recent publication of the Canada Border Services Agency’s Fees Report, available under Corporate Documents.

Place of safe-keeping

21. Goods held in a place of safe-keeping are subject to storage charges.

22. For exceptions where no storage charges are payable for goods held in a place of safe-keeping please see the Storage of Goods Regulations.

CBSA office and highway frontier examining warehouse

23. Commercial goods held in a CBSA office or a highway frontier examining warehouse are subject to storage charges, beginning on the fourth business day after the goods were left in the CBSA office or warehouse.

24. Goods will not be released until the storage charges are paid, unless the importer or broker has release prior to payment privileges. Payments made to the CBSA will be entered into CBSA Assessment and Revenue Management (CARM) system and a cash receipt will be issued as a receipt of payment. For more information on payment, please see Memorandum D17-1-5: Accounting for Commercial Goods. Where the goods have been listed on Form E44, Notice - Unclaimed Goods, the “Unclaimed Goods List” number should be referenced on a cash receipt.

King's warehouse

25. Commercial goods stored in a King's warehouse are subject to storage charges, beginning on the day they enter the warehouse. Storage charges will apply until the goods are removed from the warehouse.

26. Only in the circumstances described in subsection 6(2) from the Storage of Goods Regulations will goods be exempt from storage charges.

27. Payments made to the CBSA will be entered into CARM and a cash receipt will be issued as a receipt of payment for storage charges.

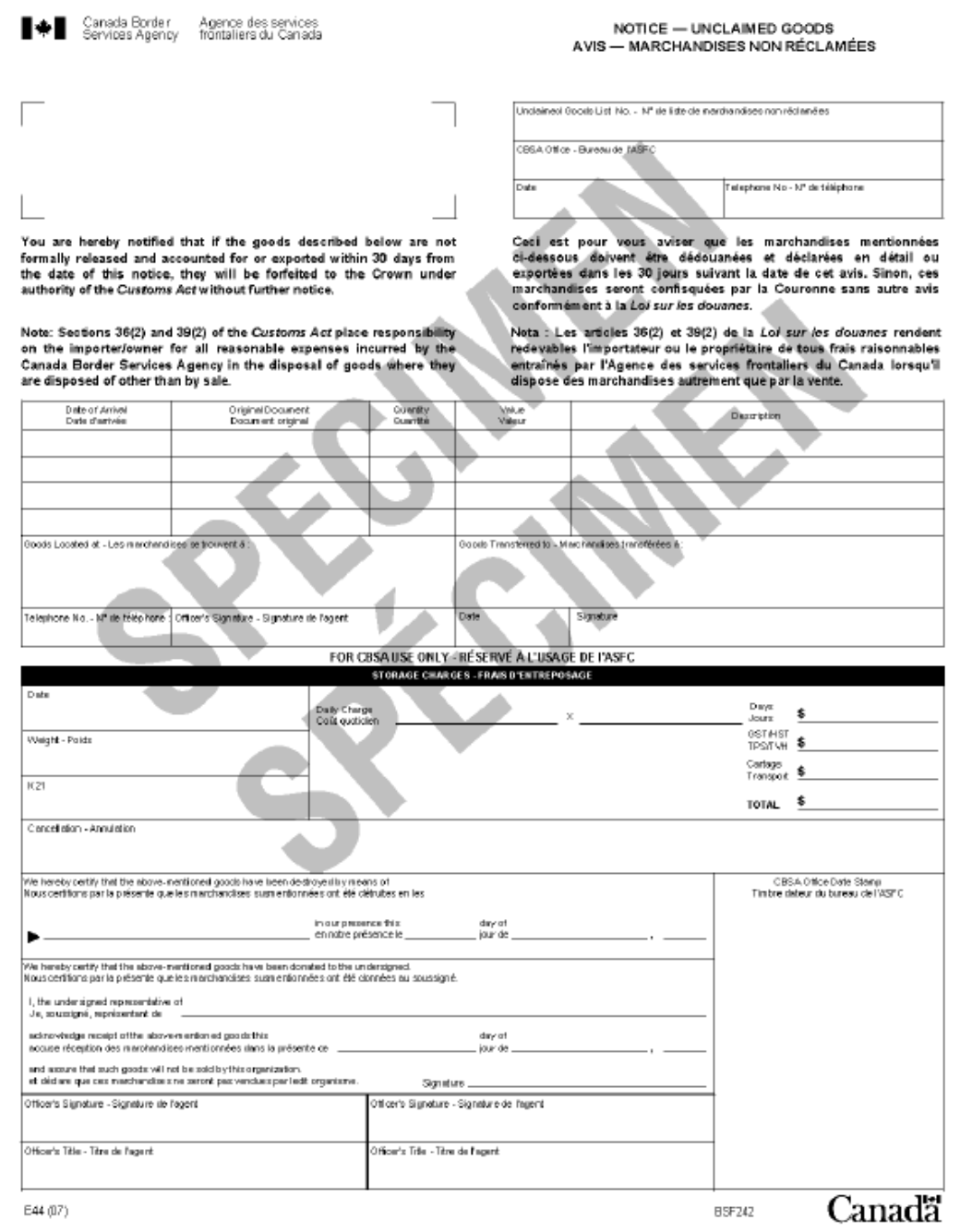

Form E44, Notice - Unclaimed Goods

28. If goods are stored beyond the time limits specified and no extension has been granted under subsection 37(2) of the act, the CBSA will issue Form E44 (Appendix A). The CBSA will send Form E44 by email to advise the importer and the carrier that the goods remain unclaimed in a CBSA office, highway frontier examining warehouse, sufferance warehouse or bonded warehouse.

29. Goods must be claimed within 30 calendar days of the date Form E44 is issued or they will be forfeited to the Crown. Once forfeit, goods are subject to disposal and can no longer be claimed by the importer or owner.

30. Goods listed on Form E44 can remain in the initial warehouse, be transferred to a King's warehouse or transferred to another location designated by the CBSA.

31. When an importer signs a certificate of abandonment for warehoused goods on Form BSF241: Non-monetary General Receipt, the goods should be listed on Form E44. Abandoned goods do not need to be kept for 30 calendar days, as the goods become the property of the Crown when the abandonment certificate is signed.

32. When goods are for immediate disposal, Form E44 does not need to be completed as goods are documented on BSF241.

33. When goods are scheduled for disposal at a later date, Form E44 should be used as a control document and Form E45 is not required.

34. Goods seized under the Customs Act, the Excise Act or the Excise Act, 2001 will only be listed on Form E44 after the legislated time frames for appeals and third-party claims have expired, or when the CBSA advises that the goods are ready for disposal.

35. A copy of Form E44 will not be sent to the importer or carrier for seized or abandoned goods, or travellers' goods held temporarily by the CBSA.

Time limits for issuing Form E44

36. For a CBSA office, highway frontier examining warehouse, or sufferance warehouse, Form E44 will generally be issued if the goods are stored beyond the 40 day limit from the date the goods were first reported under section 12 of the act.

37. However, the time limits for issuing Form E44 vary depending on the type of goods and where they are stored. The importer or broker can apply to the CBSA for an extension. For further information on extensions, refer to Memorandum D4-1-7: Extension of Time Limits for the Storage of Goods. Prescribed goods cannot be granted an extension as per section 39.1 of the Customs Act.

38. Sufferance warehouse operators must provide the CBSA with a list of goods exceeding the storage limit on the first business day following the end of the specified time limits. For further information, refer to D4-1-4: Customs Sufferance Warehouses.

39. For a customs bonded warehouse, Form E44 will be issued if the goods are on hand beyond the time limit set in the Customs Bonded Warehouses Regulations. For further information, refer to D7-4-4: Customs Bonded Warehouses.

40. Once the warehouse operator provides a list of unclaimed goods, the CBSA will issue Form E44 within five business days. The list of unclaimed goods must contain: the importer's name and address, the quantity and description of goods, the date of arrival in Canada and the cargo control number.

41. Goods that have been granted an extension will only be listed on Form E44 after the extension period has expired. For further information refer to D4-1-7: Extension of Time Limits for the Storage of Goods.

Processing by the CBSA

42. Form E44 will be numbered consecutively from the beginning of each fiscal year by the issuing office. This should be entered in the “Unclaimed goods list number” field of the form.

43. Form E44 should be cross-referenced with all previous documentation in order to maintain an audit trail for the goods. The goods included on the form must be marked with the number of goods in the shipment and the “Unclaimed goods list number” from the corresponding E44. If the goods cannot be marked, a tag may be used.

44. Once Form E44 is completed, the “Unclaimed goods list number” should be listed on Form E45. The information from E45 will serve as an audit trail from the date of receipt to the release/disposal date. This information from Form E45 can also be used if Form E44 is lost by tracking the “unclaimed goods list number,” expiry dates for disposal and to initiate follow-up action.

45. When Form E44 covers unclaimed goods, it will be distributed as follows:

- original – importer;

- copy – sent for data processing, where applicable;

- copy – held for use in the event goods are transferred to a consolidation point for disposal;

- copy – local CBSA; and

- copy – carrier.

Note: No further notification will be given to either the importer or the carrier prior to disposal of the goods.

Transfer of goods

46. When goods are transferred out of the original warehouse, they must be included on a list. The operator will sign the list approving its accuracy. Both the CBSA and the warehouse operator will retain a copy.

47. When goods are transferred to a disposal vendor, a third copy of the list will be provided. In these instances, the importer's name or address should not appear. As an alternative, goods can be identified by the list number.

48. When goods are transferred to a King's warehouse, they will be examined by the CBSA in the presence of the carrier, to confirm if there is any damage or loss.

Procedures for claiming goods prior to forfeiture

49. Goods must be claimed within 30 calendar days from when the Form E44 is issued. Unclaimed goods on hand beyond the 30 calendar days are forfeit and subject to disposal, in accordance with section 142 of the Customs Act.

50. Goods must be claimed at the CBSA office where they are being held.

51. CBSA will require the following from the importer or owner before releasing the goods:

- where the goods are to be exported:

- a cargo control document; and

- any necessary permits; or

- where the goods are to be entered for consumption:

- a completed accounting document;

- any necessary permits; and

- payment of the applicable duty and tax; or

- where the goods are to be entered into a bonded warehouse:

- Commercial Account Document (CAD);

- any necessary permits; and

- where necessary, a cargo control document.

Note: Goods that were left unclaimed in a bonded warehouse and listed on Form E44 cannot be re-entered into a bonded warehouse. They must be exported or entered for consumption.

52. Before releasing goods listed on a Form E44 from a King's warehouse, the CBSA will require:

- payment of the applicable storage charges;

- payment of any expenses incurred by the CBSA for handling the goods, for example, transportation charges; and

- written confirmation from the sufferance or bonded warehouse operator that storage charges were paid.

53. When only a portion of the shipment is being claimed, the import or export documentation should be included. If not available, an attached document must detail the number of items being claimed and the total number of items in the original shipment. For example, “entry No.16 of 20.”

Additional information

54. The Crown becomes responsible for costs against the goods from the date of abandonment or forfeiture. Sections 36 and 39 of the act make the owner or importer liable for reasonable disposal expenses where the goods are not sold. However, the CBSA may pay such expenses pending a collection action against the owner or importer.

55. Information concerning prescribed items and substances within the meaning of the General Nuclear Safety and Control Regulations can be found in Memorandum D19-2-1: Administration of the Nuclear Safety and Control Act.

Appendix A: Form E44, Notice – Unclaimed Goods

Text description

Appendix B: Form E45, Inventory Control Log for Seized, Forfeited, Detained, Abandoned, and Unclaimed Goods

Text description

References

Consult these resources for further information.

Applicable legislation

- Criminal Code

- Crown Liability and Proceedings Act

- Customs Act

- Customs Bonded Warehouses Regulations

- Customs Sufferance Warehouses Regulations

- Customs Tariff

- Excise Act

- Excise Act, 2001

- Export and Import Permits Act

- Firearms Act

- General Nuclear Safety and Control Regulations

- Nuclear Safety and Control Act

- Public Agents Firearms Regulations

- Storage of Goods Regulations

Related D memoranda

- D4-1-4: Customs Sufferance Warehouses

- D4-1-7: Extension of Time Limits for the Storage of Goods

- D7-4-1: Duties Relief Program

- D7-4-4: Customs Bonded Warehouses

- D19-2-1: Administration of the Nuclear Safety and Control Act

- D19-13-2: Importing and exporting firearms, weapons and devices

Superseded D memoranda

Memorandum D4-1-5: Storage of Goods, October 21, 2022

Issuing office

Regulatory Trade Programs and Service Transformation

Trade Programs Directorate

Commercial and Trade Branch

Contact us

For more information, within Canada call the Border Information Service at 1-800-461-9999. From outside Canada call 204-983-3500 or 506-636-5064. Long distance charges will apply. Agents are available Monday to Friday (08:00 – 16:00 local time/except holidays). TTY is also available within Canada: 1-866-335-3237.

Online enquiries can be made using the Client support contact form.

Page details

Date modified:

2026-05-21